How to Prioritize Asset Protection for Business Owners

TL;DR:

- Asset protection involves safeguarding assets from creditors and lawsuits through legal and financial strategies. Prioritizing protection begins with categorizing assets by risk and liquidity, then applying layered defenses such as insurance, legal entities, and trusts before threats materialize. Physical asset risks, like lightning damage, must be integrated into protection plans alongside legal structures for comprehensive security.

Asset protection is defined as the legal and financial practice of shielding business and personal assets from creditors, lawsuits, and operational disruptions before any threat materializes. For business owners in industrial and commercial sectors, knowing how to prioritize asset protection is not optional. A single uninsured liability claim, a lightning strike on an unprotected facility, or a missed legal formality can erase years of accumulated value. The most effective approach combines asset categorization by risk and liquidity with a multilayered defense of insurance, legal entities, and trusts, all implemented during peacetime, not after a threat appears.

How to prioritize asset protection: categorizing and assessing your assets

The first step in any sound asset protection strategy is categorization. Assets are not equal in their exposure to risk or their ease of liquidation, and treating them as equal produces gaps in coverage.

A practical tiering system works as follows. Tier 1 assets include cash, receivables, and operating accounts. These carry the highest liquidity and the highest exposure to creditor claims. Tier 2 assets cover real estate and equipment used in operations. These are harder to liquidate but represent major balance sheet value. Tier 3 assets include investment portfolios and intellectual property. Tier 4 covers speculative holdings with uncertain value and high volatility. Owners should categorize assets by risk and liquidity tiers to identify where protection gaps are most dangerous.

Statutory exemptions are the fastest and cheapest protection available. Federal ERISA law protects qualified retirement accounts with unlimited protection in many jurisdictions. That means a business owner who maximizes contributions to a 401(k) or SEP-IRA gains a legally protected asset class without any additional legal structure. Homestead exemptions protect a portion of primary residence equity in most states. These exemptions cost nothing to use and should be maximized before any complex legal tool is deployed.

Pro Tip:Before spending on LLC formation or trust drafting, map every statutory exemption available in your state. Retirement accounts and homestead protections are often the most powerful tools available, and they require no attorney.

| Asset category | Protection priority | Recommended tool |

|---|---|---|

| Cash and receivables | Highest | LLC, charging orders, insurance |

| Operating real estate | High | Separate LLC, umbrella policy |

| Investment portfolios | Medium | Irrevocable trust, DAPT |

| Retirement accounts | Pre-protected | ERISA exemption (maximize first) |

| Speculative assets | Lower | Monitor; add structure if value grows |

What are the best asset protection strategies for business owners?

Asset protection is most effective using a multilayered approach that combines insurance, legal entities, and trusts. No single tool covers every risk. Each layer handles a different type of threat.

Insurance: the first line of defense

Liability insurance is universally recognized as the first defense layer, but it must be combined with other strategies because it does not cover all liabilities. General liability policies cover common third-party claims. Umbrella insurance extends that coverage for catastrophic events and costs roughly $200–$400 per year for most business owners. That cost is low relative to the protection it provides. Insurance coverage must align with asset scale and risk, with annual review to address new exposures as your business grows.

Legal entities: compartmentalizing risk

LLCs and Series LLCs are the workhorses of business asset protection. A properly formed LLC separates business liabilities from personal assets. Segregating risk by compartmentalizing assets into multiple LLCs or Series LLCs shields other assets from a lawsuit affecting one unit. A manufacturing company with three facilities, for example, should hold each facility in a separate LLC. A judgment against one facility cannot reach the assets of the others. LLC setup costs range from $100 to $800 depending on the state.

A properly structured LLC operating agreement including charging orders and transfer restrictions is critical for legal protection effectiveness. Without strict governance, the LLC’s liability shield can fail in court.

Trusts: the deepest layer of protection

Trusts provide the strongest protection but require the most lead time. More than 19 U.S. states have adopted Domestic Asset Protection Trust laws, enabling self-settled trusts that shield assets from creditors when established before any threat arises. Nevada, South Dakota, Delaware, and Alaska are among the most favorable jurisdictions. Irrevocable trusts remove assets from your estate entirely, placing them beyond the reach of most creditors. Drafting an irrevocable trust typically costs between $2,000 and $10,000.

Pro Tip:An operating agreement is only as strong as the formalities behind it. Hold annual meetings, document decisions in writing, and never use a business account for personal expenses. Courts look at behavior, not just paperwork.

| Protection tool | Primary function | Cost range | Best for |

|---|---|---|---|

| Liability insurance | First-line coverage | $200–$400/year | All business owners |

| Umbrella policy | Catastrophic claim coverage | Varies by limit | High-exposure industries |

| LLC | Entity separation | $100–$800 setup | Operating businesses |

| Series LLC | Multi-asset compartmentalization | Varies by state | Multiple properties or divisions |

| DAPT | Deep creditor shielding | $2,000–$10,000 | High net-worth owners |

| Irrevocable trust | Estate and creditor protection | $2,000–$10,000 | Long-term wealth transfer |

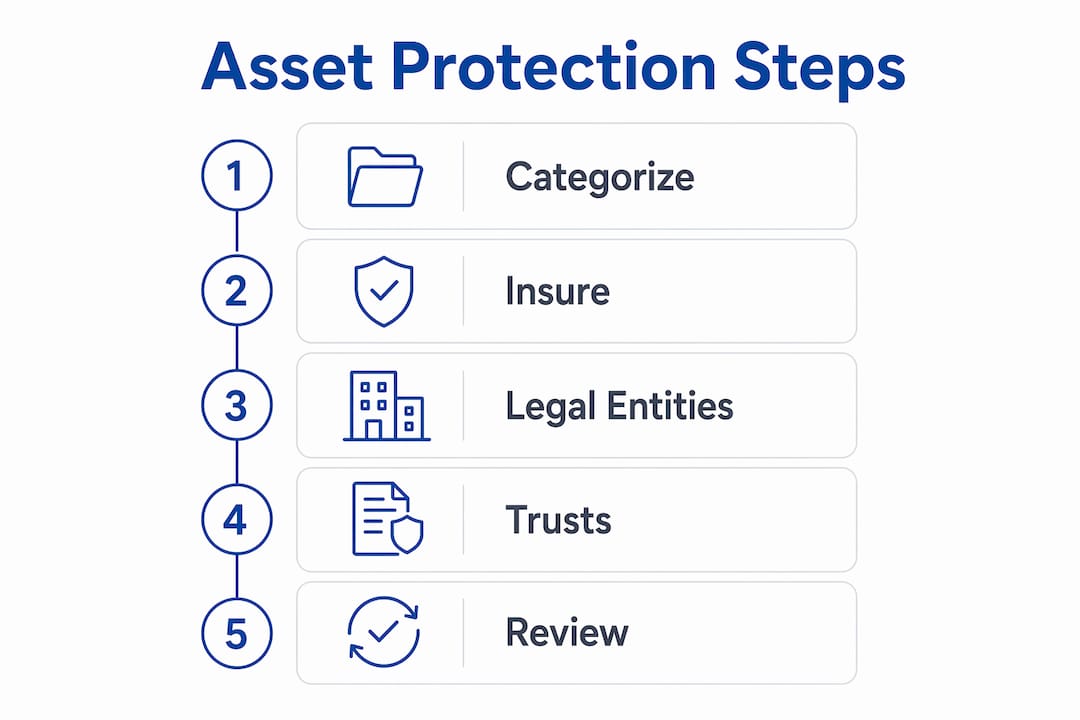

What are the steps for implementing asset protection?

A structured workflow prevents the most common mistake in asset protection: acting too late. Asset protection effectiveness depends heavily on timing. Planning must happen before any known or anticipated liability to avoid reversal under law.

Asset discovery and mapping. List every asset the business owns or controls. Include physical equipment, real estate, intellectual property, receivables, and cash. This inventory becomes the foundation for every decision that follows.

Assess risk and assign priority tiers. Score each asset by its exposure to lawsuits, natural disasters, and operational disruptions. Industrial facilities face physical risks like lightning strikes and equipment failure that office-based businesses do not. Assign Tier 1 through Tier 4 labels based on liquidity and exposure.

Optimize exemptions and insurance first. Maximize retirement account contributions under ERISA. Confirm homestead exemption status. Purchase or upgrade liability and umbrella insurance. These steps cost the least and take effect immediately.

Establish legal entities with proper timing. Form LLCs for operating assets. Consider a Series LLC if you hold multiple properties or business divisions. Draft trust documents for high-value assets you want to protect long-term. Do not wait until a creditor appears.

Maintain formalities and review annually. Periodic reviews and maintenance of protection structures are essential to adapt to evolving business and legal environments. Review insurance limits, LLC governance records, and trust terms every year.

| Phase | Purpose | Tools required | Time to implement |

|---|---|---|---|

| Asset discovery | Build complete asset inventory | Spreadsheet, accountant | 1–2 weeks |

| Risk assessment | Assign protection priority tiers | Risk framework, legal counsel | 2–4 weeks |

| Exemptions and insurance | Immediate low-cost protection | ERISA accounts, insurance broker | Immediate |

| Entity and trust formation | Legal separation and deep shielding | Attorney, state filings | 4–12 weeks |

| Annual maintenance | Keep structures legally sound | Attorney, CPA, annual review | Ongoing |

What mistakes undermine asset protection prioritization?

Most asset protection failures trace back to a small set of predictable errors. Recognizing them early prevents costly reversals.

Commingling personal and business finances. Commingling personal and business finances is the most common mistake that risks piercing the liability shield of legal entities. Maintain separate bank accounts, separate accounting records, and separate credit lines. Courts treat a business that shares finances with its owner as an extension of that owner, not a separate entity.

Relying solely on insurance. Insurance is a necessary first layer, not a complete solution. Catastrophic claims, intentional acts, and certain environmental liabilities often fall outside policy coverage. Owners who stop at insurance leave significant exposure unaddressed.

Acting after a threat appears. The Uniform Voidable Transactions Act allows courts to reverse asset transfers made after a creditor claim is known or reasonably anticipated. Transfers made under those conditions are treated as fraudulent, regardless of intent. The goal, as legal practitioners frame it, is to become judgment-proof before threats arise, making lawsuits unattractive rather than hiding assets.

Neglecting physical asset risks. Business owners in industrial sectors often focus on legal and financial protection while overlooking physical threats. A lightning strike on an unprotected facility can destroy equipment, trigger liability claims, and interrupt operations simultaneously. Physical protection layers, including lightning protection for industrial sites, belong in the same risk framework as insurance and legal entities.

Pro Tip:Schedule a formal annual review with your attorney and CPA together. Asset protection, tax planning, and estate planning interact directly. A change in one area can create unintended consequences in another.

Key Takeaways

Effective asset protection requires categorizing assets by risk and liquidity, then applying layered defenses of insurance, legal entities, and trusts before any threat materializes.

| Point | Details |

|---|---|

| Categorize assets first | Assign Tier 1 through Tier 4 labels based on liquidity and exposure before selecting tools. |

| Use exemptions before complex tools | ERISA retirement accounts and homestead exemptions provide immediate, free protection. |

| Layer defenses deliberately | Combine insurance, LLCs, and trusts because no single tool covers every liability type. |

| Timing is non-negotiable | Transfers made after a known creditor claim can be voided under the Uniform Voidable Transactions Act. |

| Maintain formalities annually | Commingling finances or skipping governance records can pierce an LLC’s liability shield in court. |

Indelec’s perspective on proactive, layered protection

The most consistent pattern I see among business owners who suffer major asset losses is not bad luck. It is delayed action. They knew the risks. They intended to set up the LLC, review the insurance, or consult an attorney. They simply waited until the threat was visible. By then, the law had already closed most of the doors.

The psychology behind sound asset protection is counterintuitive. The goal is not to hide assets. It is to become judgment-proof, meaning that pursuing a claim against you becomes more expensive and uncertain than it is worth. That posture is built during calm periods, not during litigation.

What I have found works in practice is treating asset protection as a standing agenda item, not a one-time project. Asset protection planning must integrate with tax and estate planning to avoid unintended consequences and ensure long-term sustainability. When those three disciplines work together, the protection is far stronger than any single structure can provide.

For industrial and commercial owners specifically, physical asset protection deserves equal weight alongside legal structures. A public liability framework that ignores physical risks like lightning, equipment failure, or fire leaves the entire protection architecture incomplete. The strongest defense covers every layer, from the ground up.

— Indelec

Indelec’s physical protection layer for industrial assets

Physical asset protection is the layer most business owners forget to include in their overall risk framework.

Indelec has specialized in protecting industrial and commercial infrastructure from lightning since 1955. A single lightning event can destroy critical equipment, trigger liability claims from third parties, and halt operations for weeks. Indelec’s lightning protection services cover risk assessment, system design, installation, and ongoing maintenance for facilities where downtime is not an option. When you build a layered asset protection plan, physical protection belongs in the same conversation as insurance and legal entities. Contact Indelec to assess your site’s exposure and integrate physical protection into your broader asset security strategy.

FAQ

What does it mean to prioritize asset protection?

Prioritizing asset protection means categorizing assets by their exposure to risk and liquidity, then applying the most appropriate protection tools to the most vulnerable assets first. The process starts with statutory exemptions and insurance before moving to legal entities and trusts.

When is the right time to set up asset protection structures?

The right time is before any creditor claim, lawsuit, or known liability arises. Under the Uniform Voidable Transactions Act, transfers made after a threat is known can be reversed by courts, making early action the only legally sound approach.

How does an LLC protect business assets?

An LLC creates a legal separation between business liabilities and personal assets. A properly governed LLC with a strong operating agreement prevents creditors from reaching the owner’s personal wealth in most circumstances.

What is a Domestic Asset Protection Trust?

A Domestic Asset Protection Trust, or DAPT, is a self-settled trust available in more than 19 U.S. states that shields assets from creditors when established before any threat arises. Nevada, South Dakota, Delaware, and Alaska offer the strongest DAPT protections.

Why does physical protection matter in an asset protection plan?

Physical risks like lightning strikes, equipment failure, and fire can destroy assets, trigger liability claims, and interrupt operations simultaneously. A complete asset protection plan addresses physical threats with the same rigor as legal and financial structures.